Making money is as essential to life as breathing. No matter whether you breathe slowly or fast, deep or shallow (tachypnea or chest breathing), it is compulsory if you want to live.

This is the reason money is always one of the top queries on the internet, being asked endlessly by millions every week!

If you are asked ‘How Much Money Is Enough To Live A Good Life’ to live a good life, what amount will come to mind?

$1 million? $10 million? or will you need someone else to answer it for you?

Do you really think that you need a pile of huge cash to feel like ‘Life is Beautiful’?

Let’s go ahead and figure out how much money will be enough for you, how to make it in possible ways, and whether money is the only solution to all your problems that you focus on.

How Much Do You Need to Survive a Year?

The amount of money you need to survive for a year or your whole life completely depends on the location where you live, your lifestyle expenses, and the savings and investment portfolio you wish to make for the future.

It consists of housing, groceries, food, health care, education, transportation, savings, and other essential expenses such as gas, electricity, a phone, etc.

There are non-essential expense categories too, you ‘want things’ but they are not necessary. Surely you can minimize those expenses to a possible extent, but you can’t eliminate all of them. Can you?

- Have a piece of paper with a pen and jot down the amount you spend daily on yourself. (You need to focus on this and clearly state every single payment, regardless of whether small or big.)

- Calculate your family’s (if it is, and the size of 4 members on average) monthly expenses in day-to-day life.

- You need to add your monthly savings or investment too. (if you are doing that great.)

- You should add the estimated amount you occasionally spend on parties with friends or family.

- Your travel budget and clothing expenses are on an annual basis.

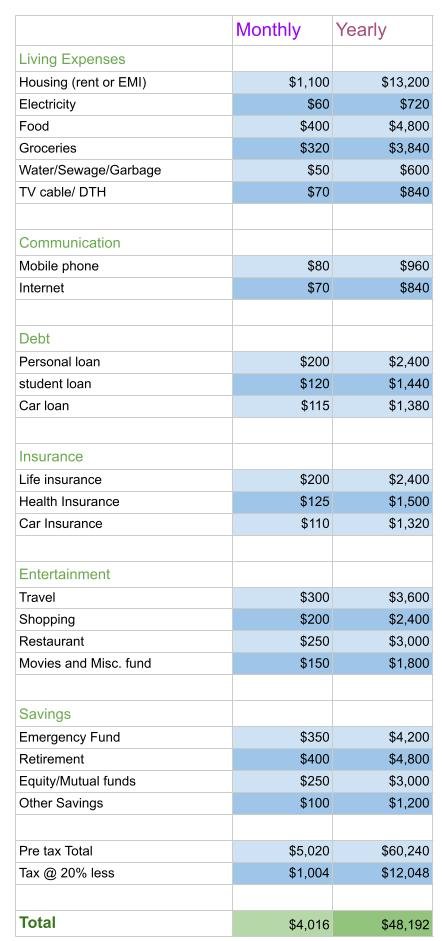

Here is a sample of a budget sheet for you to help with.

It will help you figure out the lump-sum amount you spend every month.

Though it is rough, excluding your emergency fund and any loan or debt.

Still, it is a good way to analyze your requirements for surviving a month. Multiply this amount by 12, and you will have an estimated amount for a year.

But first of all, you need to look into your yearly income left after all taxes.

If your yearly income after paying taxes is equal to or greater than this estimated amount, it is a good sign that you are on the right track. If it is not, it’s an alarm for you.

Things Affect Your Need for a Good Standard of Living.

Maybe you are happy with the current place you are living and lucky enough with the earnings you are being paid. But many people aren’t that blessed. I am sure.

Many of you must be planning to relocate and change your current source of income for the better.

In such a situation, finding the best options to adopt becomes even more important. So that you can be more precise, you need to know how much money you need to live comfortably for the rest of your life.

Your Location Matters!

First, know the area where you live. The city, town, or even countryside you live in matters a lot in terms of expenses.

Living in two different countries costs different amounts.

The same applies to living in two different cities; it will cost way differently even in the same country.

According to NUMBEO, the estimated monthly living cost of an individual (a family of four) in Kansas City, Missouri, is $3,929.8 without rent. A single person’s estimated monthly costs are $1,119.3 without rent.

The estimated monthly living cost of a family of four in New York City is $5,977.6 without rent, while a single person’s estimated monthly cost is $1,614.8 without rent.

Kansas City is approx. 30.3% less expensive than New York (without rent), you see!

It means a family of four can save almost one-third of their income if they prefer to live in Kansas City rather than New York City! And they are still citizens of the same United States of America.

Here, the cost of living describes the amount required to cover basic needs such as food, housing, transportation, and healthcare.

The figures provided by the sources are based on their estimators prepared on an average basis. Actual data may vary as it varies from city to city.

A report from the World Population Review clearly states the difference in the cost of living index among different states in America.

Where The cost of living index in Kansas is 86.5, the second-lowest in the nation. New York’s cost of living index is 148.2, the second-highest in the country.

Your Lifestyle Makes a Difference.

Not just your location of living, but your ‘Way of Living’ also affects the expenses you pay and the capital you need to acquire.

Let’s understand this more easily. To live your life, you are bound to spend on housing, food, transportation, healthcare, clothing, electricity, gas, telephone, mobile, and education.

[Debt, retirement, emergency fund, and other additional expenses are there too, but let’s aside these items for a while.]

To ‘create a style in your life’ tends to make a difference in your lifestyle expenses.

Your housing expenses will depend on the size of the house or apartment, even on the same street in the same city. Small houses have fewer rent or maintenance costs, and bigger houses will demand more money.

If you cook your food, it will be cheaper, and you can save a lot in the long run by maintaining this habit.

Ordering food online sometimes will minimize your savings, and going to have your lunch at restaurants more often will ruin your savings.

Shopping to buy your dresses during a season full of discounts will make your fund healthier; on the contrary, buying costumes from big brands will make your savings funds malnourished.

Did you get my point?

The way you choose to put money into your essential expenses has a huge impact on your lifetime earnings and, ultimately, the corpus you want to set.

Calculate- Money You Need for a Good Life.

Though we have talked about this in detail before, here we will understand how and where to calculate the estimated money you need to make to live a good life.

The amount you need to have for one year of expenses, including possible debt and savings, can be a base to start this mission.

You will need to create a spreadsheet that outlines your estimated monthly and annual expenses. Trust me, this will help you a lot.

Your Living Expenses: Housing (Rent or EMI on loan), Food, Groceries, Utilities, TV Cable, etc.

Communication: mobile, internet, etc.

Debt: student loans, personal loans, EMI on car loans, credit card debt, etc.

Insurance: health care, life insurance, car/house insurance, etc.

Entertainment: travel, OTT/cinema, shopping, parties, etc.

Your Savings/Investments

Emergency Funds: This must be a high-interest savings account (liquidity) that covers you in case of any unexpected events or emergencies (e.g., business loss or losing your job).

Many financial experts recommend having an income equal to 6–9 months of your expenses saved in this account.

Retirement plan: The day you retire from your job or regular source of income, this plan will take care of you and your family. It is wise to invest in this plan as early as possible to get maximum benefit in old age.

Equity or mutual funds: If you can and with the right knowledge of risk-reward skills, investing in the direct equity market can be a good option to capitalize on your savings. Direct index funds and mutual funds are other safer options to invest via a SIP (systematic investment plan).

Additional Savings: You can also go for short-term and long-term additional savings. They provide strong support when you plan to buy a new home or car or fuel your dreams that require money.

Here are a few methods for you to use while preparing your monthly or annual budget. These budgeting rules will help you allocate your income to the needs, debt, savings, and want categories.

What is the 50-30-20 rule?

This budgeting rule clearly states that you should spend 50% of your income (after tax payment) on your needs that you must pay for.

Remaining 30% of your income on your wants and 20% on debt repayment or savings.

This rule is a simple and general rule of thumb to promote savings and better money management. It emphasizes achieving savings goals and long-term financial security.

What is the 70-20-10 budget?

The 70-20-10 budget formula states that you must divide your after-tax income into three categories. 70% for your living expenses, 20% for debt repayment and savings, and 10% for further savings or investment.

This budgeting rule focuses on more savings and taking care of your needs (essential expenses). You can better manage your money by dividing your available income into these three distinct categories.

What is the 33-33-33 budget?

This is another budgeting rule that promotes savings and keeps your focus on expenses. The 33-33-33 budgeting rule advises you to divide your in-hand income into three equal buckets.

The first 33% of the income is for essential expenses or needs; another 33% of the income is for non-essential expenses or wants; and the remaining 33% of the income is for savings and investments.

An Average American Spends $3.3 Million a Lifetime!

Yes, you read it right. According to a new study by OneMain Financial, an average American will spend $3,356,167.80 million, to be exact, in their lifetime. The study utilized data on the average lifespan and average income of Americans.

Where do Americans spend their big money?

- On Housing: $1,486,160

- On Car: $470,000

- On Children: $467,220

- On health insurance: $290,016

- On Retirement: $195,754

- On renovations: $190,429

- On Vacations: $118,000

- On furniture: $61,630

- On Education: $42,960

- On wedding: $34,000

How Much Money is Enough for You for a Lifetime?

Before answering this crucial question, which most people ask themselves at least once, you must feed your mind with this.

There is a link between compound interest and inflation. Compound interests multiply your money over time. More longevity means better returns will be there.

While inflation is a double-edged sword, It keeps trying to destroy your value of funds over time if not taken care of and secured.

“What compound interest gives, inflation takes away.“

Why? Let’s go a little deeper to learn some more important answers.

How Does Inflation Eat Your Money?

If you are looking to build a corpus to live comfortably for a lifetime, you must face inflation. You will have to keep an eye on your savings and investment funds to see whether they are providing you with returns above inflation (which is killing your assets) or not.

Because,

1. With rising prices of goods, inflation will increase our expenses.

2. Inflation will reduce the value of our hard-earned, saved, and invested money, even without spending $1 in passing years.

Understand it this way,

Suppose Mr Modi, aged 30 years in India, spends Rs 1 lakh per month to run his family and on savings for the future.

Taking inflation at the average rate of 6% annually for the next 30 years, how much will he require per month to run his family and savings?

Well, at the age of 60, when he retires from his job, he will need Rs. 5,74,349 to bear his family’s expenses. Per month!

That’s all because of inflation.

Let’s find out the buying power of a dollar over time in the United States.

If Mr. Trump buys something worth $100 in January 2024, How much will he need to buy the same thing after 30 years under the shadow of inflation?

First, look into the inflation rate in previous years in the USA.

The U.S. inflation rate in the last 4 years

for 2023 was 4.1% (a 3.9% decrease from 2022).

for 2022 was 8.00% (a 3.3% increase from 202).

for 2021 was 4.70% (a 3.46% increase from 2020).

for 2020 was 1.23%.

taking the average inflation rate at 4% annually for the next 30 years. In 2054, Mr. Trump will have to pay $324 for the same thing. Under the impact of cumulative inflation of 224.34%.

You must keep it in mind. To tackle inflation better and knock it down, you have to invest in those funds where you not only save your capital but also increase it over the years.

How Much Money Can Make Your Life Happy?

I’ll give you a clear-cut answer to this in 2 points.

Point 1-: $1.2 million for an average American for a lifetime. While Rs. 1–1.5 lakh monthly for an average Indian.

Point 2-: No amount of money is sufficient for you unless you are content with what you have in your life.

Let’s talk about point 1 first.

According to a financial happiness survey done on Americans a few months ago, 60% of them admitted money can make their lives happy.

They just need $1.2 million in their bank account to feel financial freedom and security. Although the younger ones estimate needing more wealth, the older people are happy with less.

When it comes to salary, Americans say they need $284,167 per year to be happy.

On the other hand, from an Indian perspective, Rs. 1–1.5 lakh in monthly income is enough to be happy for an average family of four people. The cost of living in India is way less than that of its American counterparts.

Now come to point 2. Though there are surveys and public expert views, there is no exact answer that satisfies how much money is enough to live a good life or how much one needs to earn to lead a comfortable life.

Several people in India are living with their families under Rs. 15k monthly, while many white collars are struggling to do the same task even at Rs. 150k per month.

Here I am showing a video of people talking about salary related to their happiness. Hoping this will make a clear picture.

Final Words

The definition of comfort and a happy, decent life varies. But one must keep this in mind when it comes to money. More earnings will lead to more spending.

You do not need a huge amount of money to make your life comfortable.

Instead, you need to focus on your budget, where your in-hand income must be ahead of your expenses and surplus money should be invested into better-returning funds or shares.

Will you take steps to increase your income, start making a family budget, and focus on controlled expenses and more savings and investments?

Moreover, are you going to be that person who takes responsibility for his or her financial independence from now on?